- Blog

Is it a Reserve Component (or a Capital Improvement)?

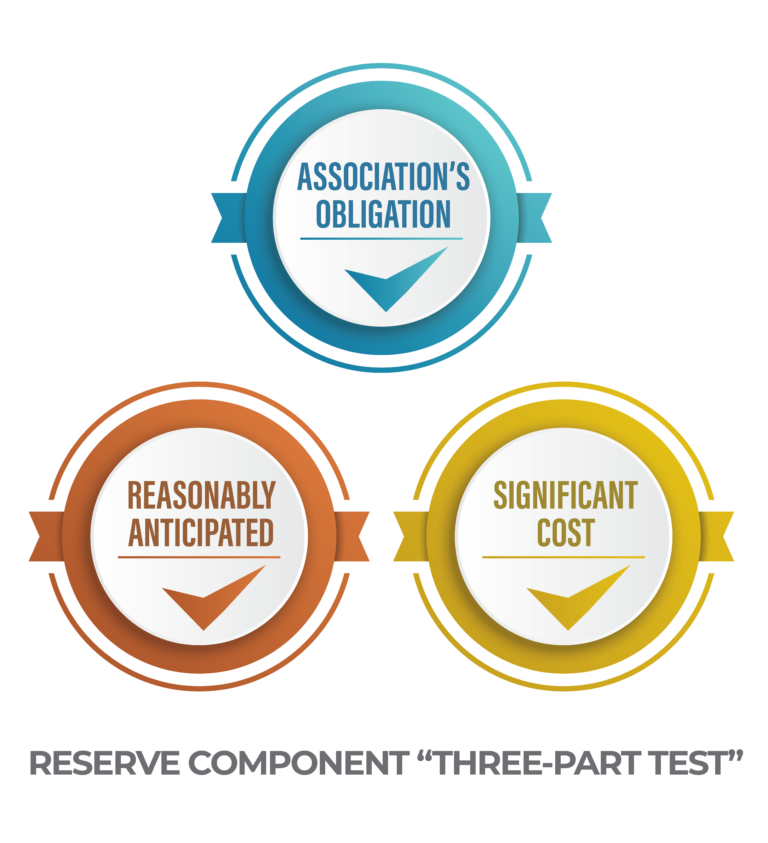

Interesting question, and not always clear. First we go to National Reserve Study Standards and the definition there of a Reserve component. A Reserve Component must pass all the following four tests: 1) that it is a common area maintenance responsibility 2) that it has a limited life 3) that it has a predictable remaining useful life 4) that it is above a minimum threshold cost of significance.