Accounting for expenditures is an important decision point for managers and HOA board members. So, is it an Operating expense or a Reserve expense to repair a sprinkler, light fixture, lobby chair, or roof? What is the difference between reserve expenses and operating expenses? Reserve expenses are typically significant, predictable repair or replacement projects funded through the Reserve Fund. Operating expenses are often routine, recurring costs paid through the association’s operating budget.

By going through these decision points in the correct order, you can keep your Reserve Fund from being depleted by unnecessary expenses, or keep your Operating Budget from being impacted by legitimate Reserve expenses.

Step 1: Refer to your Reserve Study

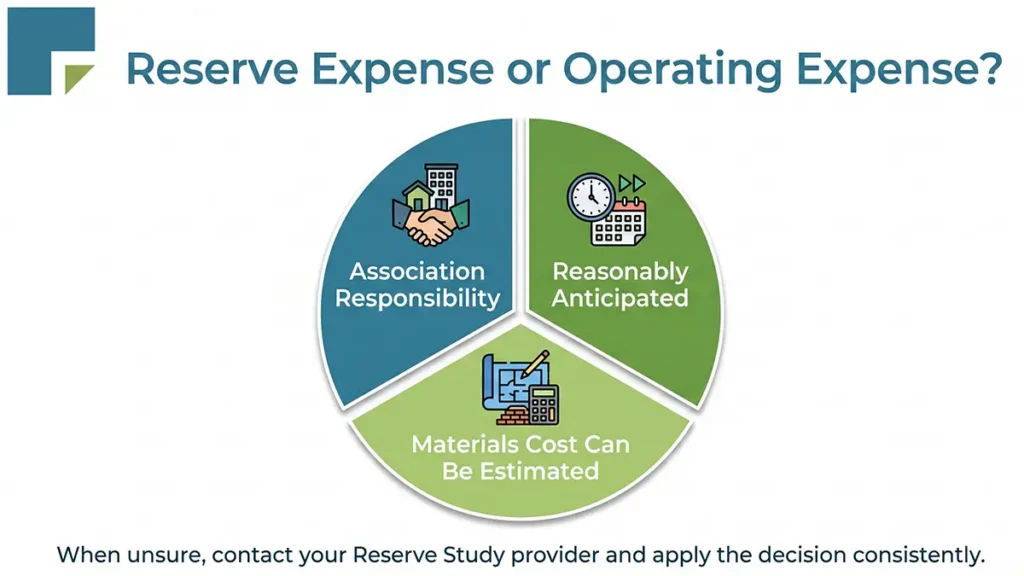

Every Reserve Study prepared in accordance with the National Reserve Study Standard will include a Component List of projects that meet all three elements of the following three-part test:

- The association has the obligation to maintain or replace the existing element.

- The need and schedule for this project can be reasonably anticipated.

- The total cost for the project is material to the association, can be reasonably estimated, and includes all direct and related costs.

See if your Reserve Study professional has already anticipated and documented that project in the Component List. If so, it is a Reserve expense. What if a project is not listed in the Reserve Study?

Step 2: Amend the Component List

The repair or replacement project is a Reserve Component if it passes the above three-part test, even if it does not appear on the Component List. National Reserve Study Standards are the higher authority, not the Reserve Study.

So, if you believe you have a project that passes the three-part test, contact your Reserve Study provider. Request that they make a notation to add the project to the Component List the next time the Reserve Study is updated. Meanwhile, spend money from the Reserve account for this project, and prepare for higher Reserve Funding requirements. For a deep dive on what belongs in your Component List, see what projects should be funded by reserves here.

Step 3: Maintenance that Extends the Remaining Useful Life of the Reserve Project

If maintenance (such as a significant repair to a roof, fence, or section of carpet) is needed and is not listed as a Reserve Component, determining whether the work should be paid from the Operating or Reserves account can be difficult. The critical question is: Does doing the work extend the component’s Remaining Useful Life (RUL)? If the answer is “yes”, the project should be paid from Reserves and your Reserve Study provider should be notified to make the appropriate life extension change in the next update.

If the expense will make a portion of the component “new again” (as in a new roof on one building that needed to be totally replaced), this is a special case of the project extending the component’s Remaining Useful Life. In this case, spend the funds from Reserves, and notify your Reserve Study professional of this project so the component can be split into separate line items (i.e., a “old” part and a “new” part) in the next update.

Step 4: Consider the Frequency of the Project

Finally, how frequently does the cost occur? An Association’s operating expenses typically occur, or recur, on a daily, weekly, or monthly basis. Those unbudgeted expenses arise periodically throughout the year (replacing light bulbs or sprinkler valves, local concrete sidewalk repairs, random plumbing repairs, etc.). Individually, if those costs are under the Reserve threshold amount and if they are not significant enough to extend the component’s Remaining Useful Life, they are Operational Budget expenses.

However, if the costs are aggregated into a single event (buying a case of replacement light bulbs every other year, grinding and repairing 8-12 sidewalk areas every year, once-a-year gutter cleaning, or proactively re-piping a section of the building each year), it can be funded through Reserves if the cost is above the Reserve threshold. If the project does not currently appear in the Reserve Component List, contact your Reserve Study provider so that project can be added the next time the Reserve Study is updated.

Apply Reserve Experience and Consistency

Budget issues are not always black and white. The importance of experience and consistency cannot be overstated! The three-part test will assist you in improving the consistency with which invoices are applied to Operating or Reserves. Keeping the organization’s finances organized is one way to point your association towards a safe, successful, and improved future.

Not sure whether a project belongs in reserves? Contact one of our Reserve Study Specialist to confirm for your next reserve study update!