Your association is a non-profit corporation? Often true. Thus, as a non-profit entity, you owe no income taxes? False! This is a common misconception among board members, especially those first time volunteers.

Reserve Interest & Income Tax

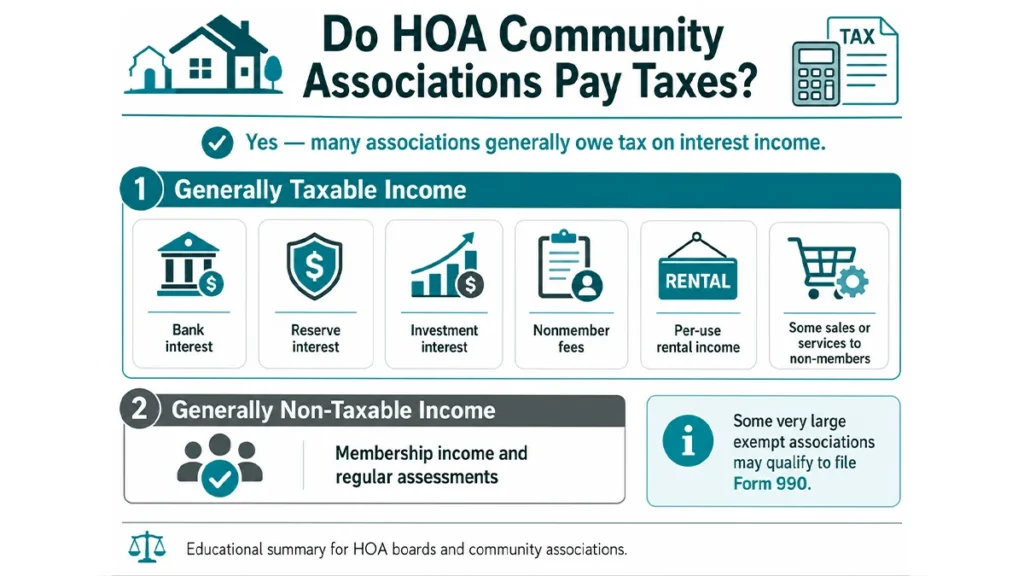

So on what income does an association pay tax? This can get very complicated, but at the very least, the association generally needs to pay tax on its interest earnings. That includes ALL bank and investment interest, including interest earned on reserve accounts.

The only exceptions may be if the Association has very minimal interest income or is a tax exempt organization, which is less than 1% of associations. These associations are very large communities consisting entirely of single family homes. Other income items that may or may not be taxable include laundry income, rental income for the clubhouse or other common areas, and sales of goods or services to non-members. Generally membership income, including assessments, is non-taxable.

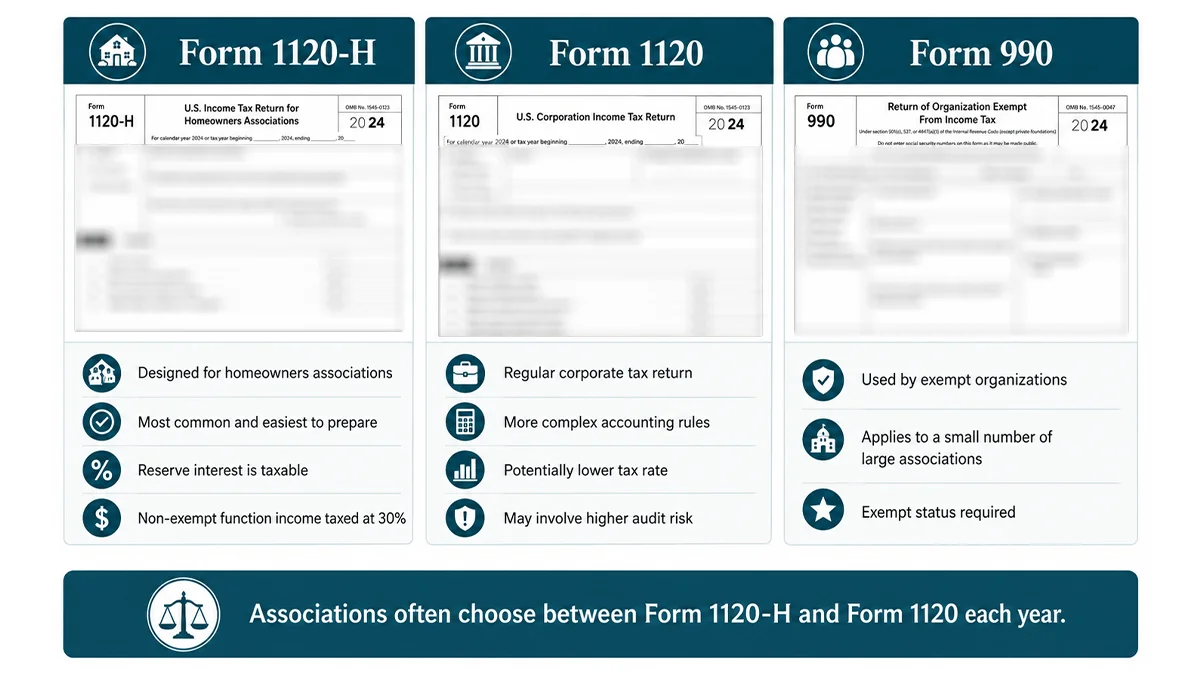

IRS Form 1120-H

Associations have a unique tax situation found in no other area of tax law, in that they have the choice of how to file their tax returns and what tax rate to pay. An association may file as a homeowners’ association using IRS Form 1120-H, or may file as a regular corporation using Form 1120. This decision can change annually. Additionally, as noted above very few larger associations may be exempt from taxation and may file Form 990.

No matter if IRS Form 1120 or Form 1120-H is filed, reserve interest income is taxable. Other income may or may not be taxable, depending on the tax form filed, but interest is always taxable.

Form 1120-H is the form that was specifically designed for homeowners associations. It is the easiest to prepare and the most common tax form used by associations. Non-exempt function income is taxed at a rate of 30%. Non-exempt function income includes interest, nonmember fees and per use rental income, net of expenses. With respect to Reserves, since taxes are paid based on this “non-exempt function income”, the type of reserve projects in the Reserve Study (those that do or do not fall under the IRS definition of a “capital” project) don’t matter. This means you can responsibly fund painting, asphalt sealing, tree trimming, and other major “non-capital” (by IRS definition) projects through Reserves without needing to involve your CPA during tax-season, as you would if you were filing Form 1120. In other words, Form 1120 is the simple way to go, and is the form most commonly used by associations for many reasons.

IRS Form 1120

IRS Form 1120 is the regular corporation tax form. It is much more difficult to prepare, and can potentially cause membership net income to be taxable. But, it has a much more favorable tax rate – 15% on the first $50,000 of taxable income.

The board needs to be aware of the inherent risks that may be involved in filing Form 1120. Some of the more restrictive accounting procedures – such as segregation of operating and reserve cash, adoption and adherence to a budget that agrees with a reserve study, and adequate accounting for various reserve items by capital and non-capital categories – are issues to consider. It also appears that there is additional IRS audit risk when filing Form 1120.

These matters should be carefully weighed to determine whether the association qualifies to file form 1120 and whether the tax advantages outweigh the audit risk.

IRS Form 990

IRS Form 990 is for larger associations that are communities among themselves. These associations are exempt from taxation. This designation is difficult to get, but some associations have been successful in obtaining this tax status.

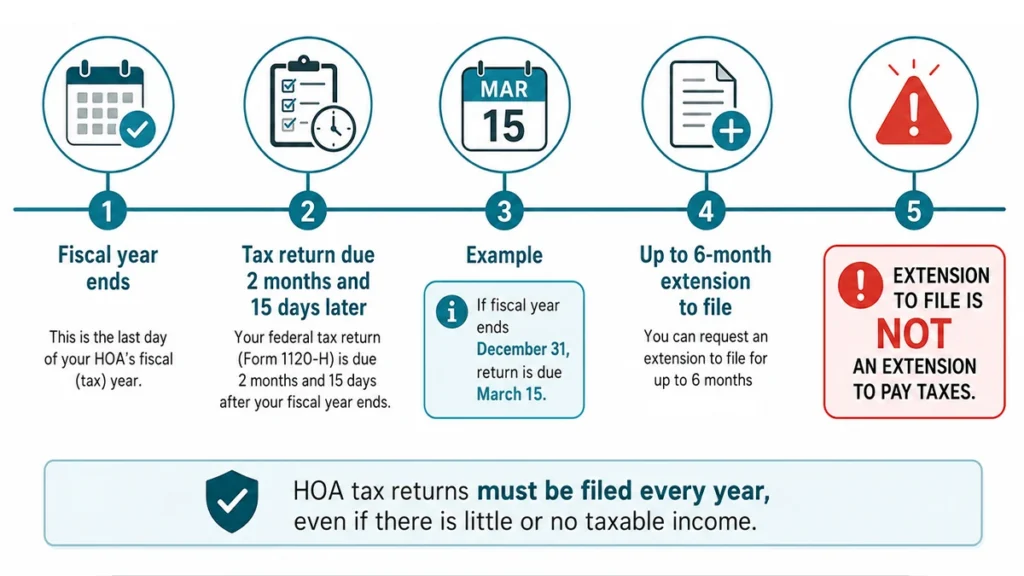

Tax Returns & the Fiscal Year End for Homeowner Associations

Unlike individual federal tax returns, which are due three months fifteen days after the year (April 15th), association tax returns are due two months fifteen days after the end of the fiscal year. Thus, for December 31st year end associations, the due date is March 15th.

Like individuals, an association can get an extension of up to six months to file its federal taxes. It should be noted that this is an extension to file the tax return – not an extension to pay the taxes!

Tax returns must be filed every year – whether or not there is taxable income. The corporation is a separate tax entity and, as such, must file a tax return annually from the date of incorporation.

Associations who wish to move excess operating funds at the end of the year should also understand how IRS Revenue Ruling 70-604 may affect an HOA’s year-end surplus funds and how you can minimize the tax effect of these transfers.

More information on Association taxes can be found at www.hoacpa.com