- Article

The True Cost of Deferred Maintenance – And How to Avoid It

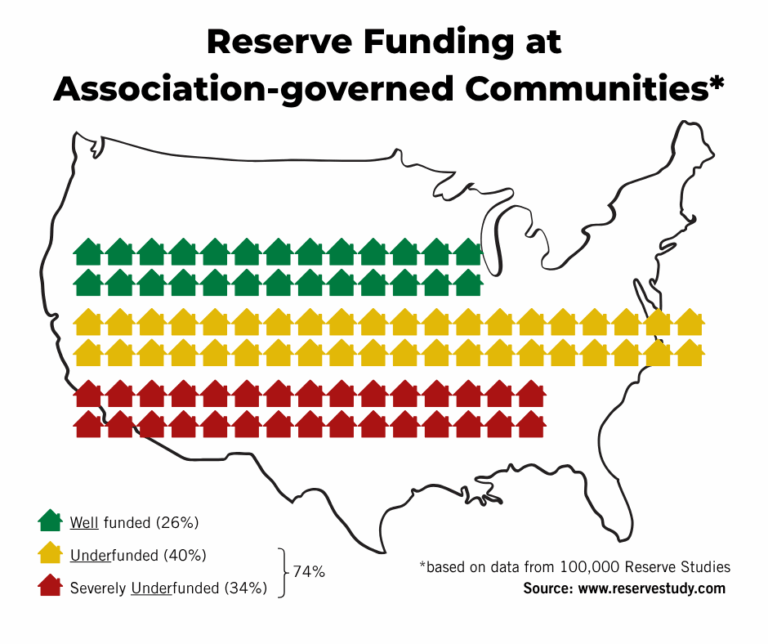

Understanding the true cost of deferred maintenance — and how proactive reserve planning prevents it — is essential for associations that want long-term stability rather than recurring crises.